Every organization immediately after its creation is required to keep accounting records. According to the law of December 6, 2011 No. 402-FZ, accounting and storage of documents is organized by the head of the LLC. The director is responsible for organizing accounting in the organization, and even financial statements are recognized as drawn up after the signature of the director, and not the chief accountant. Entrepreneurs are luckier in this sense - it is not required by law.

Accounting is the organization of collecting information about the state of the property and obligations of the company, as well as the continuous reflection of this information in special accounting documents. But LLC accounting is not only registers, accounting books and financial statements. These are also tax accounting documents, contracts, personnel and primary documentation, documents on cash flow (cash and bank). We have collected the entire extensive list of documents that need to be maintained in an LLC in the article "".

Please note: for violation of accounting rules. Accounting support services are not something you should save on, especially since they will not require any special expenses.

Is it difficult to keep books for an LLC? The answer to this question will depend on several factors:

- Selected tax regime. It's enough to just keep track of USN Income and UTII. It’s more difficult - using the simplified tax system Income minus expenses. The most difficult thing will be accounting for common system taxation.

- Availability of employees. Reporting for employees is complex and voluminous; in addition, it is necessary to prepare salary calculations and payment of insurance premiums every month, and, if necessary, also vacation pay, sick leave, and maternity payments. But even if there are no employees, and the only founder runs the organization without employment contract, must be taken zero reporting. In addition, all organizations, even those without employees, must annually submit information about. And new organizations must submit it no later than the 20th day of the month following the month of registration.

- Number of operations. These are any business actions that have changed the ratio of income and expenses of the organization: receipt of payment from customers, payment of wages, purchase of goods, etc. The more transactions there are, the longer it will take to complete them.

- Diversity of activities of the organization. There are specific accounting features in certain areas of business (trade, production, services, construction, etc.). It is easier to account for operations of the same type than to combine accounting for different areas.

- Category of your partners. If you and your counterparty work under different tax regimes, if you plan to conduct foreign economic transactions or work with budgetary or state-owned enterprises, then the accounting will have its own peculiarities.

But even in the simplest version - the absence of employees, a small number of operations, choosing the simplified tax system Income or UTII mode - accounting for an LLC will require professional knowledge or the use of specialized programs. Accounting services for an LLC can be entrusted to a full-time employee or a specialized company. - this is a complete or partial transfer of accounting responsibilities to a professional independent contractor.

Accounting statements of LLC

Accounting in an LLC must ensure the completeness of collection and recording of information about the financial activities of the organization. Where to start with LLC accounting?

Step 1. Determine who is responsible for maintaining accounting records at the enterprise. Often, after registering a company, the director assigns the responsibilities of the LLC accountant to himself. At first, this is a completely acceptable situation, but as soon as the deadline for submitting any reports approaches, you need to either figure out this issue yourself or transfer the service to specialists.

Step 2. Choose you will work. This must be done immediately after registering the LLC, or better yet, before you submit the documents to the Federal Tax Service. When choosing a regime, we recommend that you receive a free tax consultation, which will help you save significantly on payments in your budgets. Under different regimes, the tax burden of the same enterprise can differ significantly!

Step 3. Review your regime's tax records. On the simplified tax system you need to submit only one declaration at the end of the year, on UTII, quarterly declarations, on OSNO, every quarter you submit declarations on profit and VAT and an annual declaration on property tax.

Step 4. Develop and approve organizations.

Step 5. Approve the working chart of accounts. The document should be based on the chart of accounts developed by order of the Ministry of Finance of Russia dated October 31, 2000 N 94n.

Step 6. Organize your accounting primary documents and reflection of the information contained therein in the accounting registers.

Step 7 Comply with the chosen tax system and reporting for employees.

Our users can receive a free month of accounting services provided by 1C:BO specialists with the transfer of the 1C Accounting information base after the end of the trial period.

Law No. 402-FZ includes a balance sheet, a statement of financial results and appendices to them as the financial statements of an LLC: reports on changes in capital; cash flow; on the intended use of the funds received (if they were received).

Balance sheet and profit and loss statement of the enterprise

The forms of the enterprise’s balance sheet and LLC’s profit and loss statement were approved by Order of the Ministry of Finance dated July 2, 2010 No. 66n. Later, by order of the Ministry of Finance of Russia dated 04/06/2015 No. 57n, the profit and loss statement was renamed to the financial performance statement. Organizations are required to submit financial statements at the end of the year, no later than March 31 of the following year. But investors, creditors, banks, and counterparties have the right to request a report on financial results during the year, so you can make a snapshot of the financial condition of the LLC based on the results of the quarter or month.

The LLC balance sheet form can be found in appendix. No. 1 to Order of the Ministry of Finance of July 2, 2010 No. 66n. This is the so-called full balance on two pages.

Accounting statements of an LLC using the simplified tax system in 2019

How to keep accounting records for an LLC under the simplified tax system Income 6% and under the simplified tax system Income minus expenses? The simplified taxation system involves submitting just one annual tax return. Its shape is the same for both versions of the simplified system.

What financial statements do LLCs submit to the simplified tax system in 2019? Keeping accounting records under a simplified taxation system allows you to submit financial statements in a simplified form (Appendix 5 to Order of the Ministry of Finance dated July 2, 2010 No. 66n). It includes only the balance sheet and income statement. If the organization received targeted funds through the simplified tax system, then they also need to be reported. It is not necessary to submit reports on changes in capital and cash flows.

An example of filling out a simplified balance sheet of an LLC using the simplified tax system:

Accountant services for LLC

Let's summarize. Accounting services for LLCs are mandatory in all tax regimes and even in the absence of real activity of the company. Bookkeeping can be done by the manager himself, a full-time specialist, or a specialized outsourcing company. for an LLC will depend on the volume of work: the number of business transactions, the complexity of the chosen mode, the number of employees, and the method of accounting.

For our users who want to do their own accounting for an LLC, we want to offer the 1C Entrepreneur online program. This is a completely new tool for increasing business efficiency, which allows you to:

- maintain full accounting and tax records;

- carry out settlements with counterparties;

- issue and pay invoices and payment orders;

- calculate any payments to employees;

- save all LLC documents in a single database;

- analyze sales, income and expenses;

- choose the minimum possible tax burden, etc.

Andrey Kryukov’s book “Accounting from Scratch” will help everyone who wants to understand such a complex area as accounting. It is suitable for beginners and entrepreneurs. Many who decided to study accounting on their own quickly stopped, realizing that it was almost impossible to navigate it. And this is exactly what it seems to those who have no idea what it is.

With the help of this book, it will be easy to understand the basic terms and concepts, which are explained here in accessible language. You will understand the difference between debit and credit, how cash flows in the company. You will learn how accounting in an organization is regulated by the state, how taxes are related to it, what inventory is, how to evaluate expenses and profits. You will learn to understand accounts and postings and will be able to prepare them yourself after some practice. The book provides knowledge about the tasks of accounting, its principles and techniques. Gradually immersing yourself in the specifics of accounting, you will learn to feel confident in doing the necessary work, which will no longer cause misunderstanding and rejection.

On our website you can download the book “Accounting from Scratch” by Andrey Vitalievich Kryukov for free and without registration in fb2, rtf, epub, pdf, txt format, read the book online or buy the book in the online store.

Accounting is a complete and continuous recording of an organization’s activities based on and registration of business processes in monetary terms. Everything is conventionally divided into two parts: assets (funds that belong to the enterprise) and liabilities (sources of these funds). Knowing the chart of accounts represents the basics of accounting. All transactions are reflected. Thus, the acquisition of fixed assets, the receipt of money in the current account is reflected as a debit, that is, an increase in assets occurs. The decrease in assets is shown on the credit of accounts. An increase in a liability is reflected as a credit, and a decrease as a debit.

All postings are made on the basis of instructions from the Ministry of Finance and the Tax Service and only in the presence of primary documents (invoices, contracts, invoices). Understanding the basics of accounting is essential to the day-to-day work of all financial professionals. When drawing up entries, it is important to logically take into account that an increase in the organization’s funds (assets) must be recorded as a debit, and a decrease in them - as a credit. An increase in the enterprise's sources of funds (liabilities) is indicated as a credit, and a decrease in sources - as a debit.

The fundamentals of accounting are two principles:

- The principle of balance

The principle of accounting balance is based on the formula:

ASSETS = LIABILITIES + EQUITY

ASSETS are everything that a company has and uses to make a profit.

LIABILITIES are everything that an enterprise owes to external investors, suppliers, government organizations and the budget.

OWN CAPITAL is the part that remains when liabilities are subtracted from assets. This shows that LIABILITIES are paid off first upon liquidation or closure of the enterprise, and each owner can dispose of OWN CAPITAL last.

- Double entry principle

All financial transactions have offsetting sides, but the principle of balance must always be respected. For example, you have 100,000 rubles, but you need to purchase equipment for 300,000, then you take out a loan from a bank for the missing amount.

A(100000)=O+ SK(100000)

In accounting, this operation is recorded as a debit to the cash desk - 200,000 rubles and a credit as an obligation to the bank - 200,000 rubles.

A(100000+200000)=O(200000)+CK(100000) Thus, the principle of balance is preserved.

Particular attention should be paid to expenses in accounting. Expenses are primarily a decrease in economic benefit in a given period, as a result of an outflow of assets or an increase in liabilities, which leads to a decrease in capital.

An accountant should not confuse costs and expenses in accounting and should always understand their differences during work and be able to competently defend their point of view before the audit authorities. Expenses never reduce OWN CAPITAL, unlike expenses. The company incurs costs for a certain period, then these costs turn into ASSETS or expenses. Expenses depend on costs and always affect the profit of the enterprise. But the costs themselves do not affect profits.

I will show with examples: Repayment of accounts payable leads to a decrease in ASSETS (money paid), but at the same time LIABILITIES also decreased (debt is repaid), which means that OWN CAPITAL has not changed. Therefore, it is incorrect to consider this an expense.

Writing off accounts receivable after the expiration of the three-year statute of limitations is an expense, since there is a decrease in ASSETS without a change in LIABILITIES, which means that OWN CAPITAL decreases. Similarly, you can recognize as a negative expense or recognition of fines, penalties, and state fees.

Costs for leasing property are an expense at the end of the period; costs for production that closed and did not make a profit can also be considered an expense.

That's actually all the basics of accounting, based on logic, and not on special instructions, methodological manuals, regulations and other regulatory documents. In accounting, you need to think logically and not just blindly follow requirements.

An accountant is a specialist on whom the financial well-being certain company. A person who wants to become a professional in the field of accounting needs to regularly make various calculations. Real specialists also understand the basics of economics and communication.

First of all, a person must ask himself the question of whether he is ready to connect his life with important but routine work. The profession of an accountant does not imply creativity or even a regular change of environment. And you need to be mentally prepared for all this. You can’t choose a profession based on the principle: “just so long as it takes.”

First of all, a person must ask himself the question of whether he is ready to connect his life with important but routine work. The profession of an accountant does not imply creativity or even a regular change of environment. And you need to be mentally prepared for all this. You can’t choose a profession based on the principle: “just so long as it takes.”

If a person is serious about becoming an accountant, then there are two options for the development of events:

- Homeschooling. You can “attend” webinars, take online courses, read books and articles. You definitely need to master, in particular, C1. There are now many resources and opportunities available for a self-study student.

- Studying at a higher educational institution. In principle, the accounting profession is provided in many colleges, so people with 9 years of education can also go to study. But later you will still have to get a higher education, since this is more valued among employers.

It is worth considering that a self-taught accountant will also need to undergo practical training. Not every company needs personnel without a diploma and recommendations, so you will have to try hard to get the desired position. It is recommended to take training courses to obtain a certificate.

A true specialist constantly improves his skills, masters new programs and monitors specialized literature.

Is it possible to become a professional at home? Yes, you can. But you should understand that without the appropriate education it will be much more difficult to find a job. Therefore, it is recommended to study at colleges, universities and universities. A person with “crusts” can be firmly confident that he will not be left without work.

An accountant is a specialist who controls the losses and profits of a particular company, as well as prepares financial documentation.

An accountant is a specialist who controls the losses and profits of a particular company, as well as prepares financial documentation.

There are representatives of this profession in every organization: commercial, public, government.

Accountants work in a special system (1C), which allows them to organize all the necessary information and make calculations.

The responsibilities of accountants include the following tasks:

- calculation of production costs and profits received;

- control of financial discipline;

- preparation and submission of reports on the financial condition of the organization;

- issuing wages to employees;

- interaction with tax companies.

Not all accountants perform a large volume of tasks. It all depends on the turnover and size of the company, as well as its field of activity. Many organizations employ a whole staff of accountants. Every professional is engaged specific tasks: for example, issued to employees wages or calculates total expenses for the month.

Every company, even the smallest one, needs accountants. Since 2013, the need for accounting according to the simplified tax system was introduced, which made the profession even more in demand. Now even small business owners are required to have an employee responsible for financial and tax reporting.

What qualities does an accountant need? First of all, the ability to perform monotonous paperwork. Also, representatives of this profession must be sociable, intelligent and resourceful. It depends on them whether the company will stay afloat (especially if it has recently opened). Accounting professionals are highly valued and well paid.

There are many specific terms and definitions used in the accounting field. A novice accountant must master the basic terminology:

The LIFO method of estimating the cost of goods is prohibited and has not been used since 2008.

This is not all the terminology that is used in the field of accounting. The remaining definitions can be learned from books or during training. educational program. It is extremely important to know the basic terms as they help you understand the basics of accounting as well as reporting.

Accounting training for 2018

There are many options for studying accounting in 2018. You can learn a profession through webinars or get a full-fledged education at an educational institution, and then take advanced training courses.

There are many options for studying accounting in 2018. You can learn a profession through webinars or get a full-fledged education at an educational institution, and then take advanced training courses.

Modern companies need professionals who keep up with the times.

You can master your specialty at a college or university. It is best to choose educational institutions located in Moscow or St. Petersburg.

In the central cities of Russia the most high level education that meets all necessary requirements. You can study to become an accountant at the following universities and universities:

- MATI;

- University of Humanities and Economics;

- MNEPU (non-state academy);

- Academy of Management and Business (international);

- Institute of Business and Law.

The list includes leading educational institutions in Moscow. The specialty that will need to be mastered is called accounting, analysis and auditing. After obtaining a diploma, a person can also become an economist.

Homeschooling is suitable mainly for those who do not want to connect their lives only with accounting activities. Mastering a profession at home will take a minimum of time if a person approaches the process responsibly.

Supporting literature (all books published in 2016):

- Accounting and analysis. Authors: Eremina and Rachek. The book consists of 2 sections. The first contains information about the development of accounting in different time periods, starting with ancient world. The second section includes a description of the various accounting methods.

- Accounting theory.

- All about tax audits. Authors: Sukhovskaya, Myrtynyuk, Sharonova. As mentioned earlier, accountants constantly have to deal with tax inspectorates. This book describes in detail which aspects of a company's activities are most often inspected by inspectors.

These manuals are the most informative and new. It is also recommended to read books such as: Accounting in 10 days (2012), Workshop on accounting (2010). They contain useful and relevant information, despite the fact that they were released quite a long time ago.

Exists five forms of financial statements:

- Balance— reporting on the financial condition of the enterprise for a specific period of time. It is calculated using a form (table) consisting of two parts: the first contains information about the company’s liabilities, the second - about assets.

- Loss and Profit Report— information that allows you to display the results of the financial activities of an enterprise for a specific time period. When drawing up a document, you must indicate all information about the organization’s income, even if the revenue was not received from the main activity.

- About budget (capital) changes. The document must be filled out based on letter of the Ministry of Finance No. 117 (dated December 23, 1997). It is important to adhere to the basic provisions in order to correctly prepare reports. All information about capital should be indicated step by step, using not only general data (about use and receipts), but also information about cash balances on the account.

- About cash flow. The reporting indicates data on funds received and spent for the year. At the same time, all amounts are divided into several parts corresponding to the current, financial and investment activities of the organization. The goal of current activities is to obtain maximum profit from the sale of goods or services. Investment cash movements are associated with the purchase or sale of equipment, real estate, and assets. Financial activities are called financial activities that do not greatly affect the overall budget of the company.

- . The document must be filled out in accordance with the requirements set out in Letter of the Ministry of Finance No. 4n (dated January 13, 2000). The letter contains information about all forms of accounting. reporting of organizations.

All documents must be drawn up correctly, since the main activity of the enterprise depends on this. If the accountant makes a mistake in the calculations, the company may suffer large losses.

Primary documentation is papers that are needed primarily for reporting to tax companies. They are stored for 4 years.

TO primary documentation relate:

- sales receipts and invoices;

- certificates of services performed;

- cash receipts;

- expense reports;

- current account statements;

- documents confirming payments to employees;

- statements and limit-fence cards.

Primary documentation is drawn up in a generally accepted form or on forms developed by the organization itself.

How long does it take to study to become an accountant? People who have completed 9th grade will need 3 years and 10 months to master a profession in college. Training based on 11 classes will take 2 years and 10 months.

How long does it take to study to become an accountant? People who have completed 9th grade will need 3 years and 10 months to master a profession in college. Training based on 11 classes will take 2 years and 10 months.

In some educational institutions An accelerated program is provided. You can study it in 2 years and 10 months (based on 9 classes) or in 1 year 10 months (based on 11 classes).

There are also special courses, the duration of which rarely exceeds 6 months. On average - 2.5-4. You need to choose your courses carefully, as some people teach with an outdated or incomplete curriculum.

The duration of home study directly depends on a person’s abilities and his desire to master a specific profession. Some people learn completely in a year, while others take 3-4 years.

How long will it take to become a chief accountant? Man with higher education can apply for this position after 3 years of work in one company.

A lecture on accounting for beginners is presented below.

Accounting is a very important concept within the discipline. And if you have to study it because of your studies, let’s figure out together what accounts are, why they are needed and how to use them?

Account Definition

Let's try a popular science explanation of what accounting accounts are for dummies.

Accounts are a method of cumulative interconnected reflection and grouping of property by location and composition, by sources of its formation, as well as a method of business transactions according to qualitatively homogeneous characteristics, expressed in natural, labor and monetary measures.

This is an official and very complex definition. Let's say more in simple words: These are tables with 2 columns: left (debit) and right (credit). This table allows you to see all the operations of the enterprise that occurred during the month.

Receipts to the enterprise account are reflected on the left, and disposals are taken into account on the right. The numbers displayed in the table are equated to monetary terms.

Within the enterprise, many different business transactions are carried out every day: the receipt of funds and their disposal, salary payments, payment of taxes and much more. All these operations are usually grouped by common features. Each group belongs to a specific account.

For example, any operations to record material assets belong to account 10 (materials). Any cash transactions relate to account 50 (cash), etc.

On a note!

In total, 99 accounts are allocated in accounting, each of which can be viewed in the “Chart of Accounts” document.

Chart of accounts: teach or hang yourself?

Students think that it is easier to commit suicide than a chart of accounts. In fact, this is a very useful document.

In addition, there is absolutely no need to memorize it, no matter what your teacher tells you. The fact is that any business uses only a few of the most frequently used accounts in its business, so you won’t even need many of the accounts.

Reinforcing knowledge with examples

Let's look at an example of how an enterprise keeps records of its household. activities using accounts.

At the beginning of each month, the company maintains a new account. account, opening a new plate. At the very beginning of each table, the remainder (balance) from the previous month is transferred. If the balance was debit, it must be entered in the debit column, if it was credit, then in the credit column.

Then, throughout the entire month, the table reflects all ongoing business transactions.

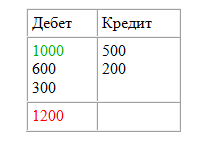

As an example, let's take an organization that maintains 51 Current Account.

At the end of last month, the organization’s account had 1,000 rubles remaining (closing balance). This 1000 rubles must be entered at the beginning of the table, account 51.

Over time, the company has carried out various monetary transactions, adding and subtracting money from the account, and all of them are reflected in the table.

By the end of the month, you should calculate the cash turnover during the month - that is, simply add up the values of each column. And then we calculate the final balance - add to it all the numbers in the debit column and subtract from the resulting amount general meaning credit column.

If the resulting figure comes out positive (with a + sign), it is considered a debit and is recorded in the debit column for the next month. If the final balance is negative, it should be recorded in the table in the credit column.

The balance was calculated, the account was closed, and at the beginning of the next month we opened a new one and proceed according to the usual pattern.

And here you can watch a video on the topic of accounts in accounting for dummies:

You might find a sample year helpful. Well, if you have a very difficult test or coursework on accounting and auditing, they will not only try to explain it to you briefly and clearly current topic, but are also ready to complete this verification work for you in the shortest possible time.